![]()

Pass PRMIA 8011 With Prep4SureReview Exam Dumps - Updated on Sep-2025

Fully Updated 8011 Dumps - 100% Same Q&A In Your Real Exam

NEW QUESTION # 144

Which of the following statements are true:

I. Credit VaR often assumes a one year time horizon, as opposed to a shorter time horizon for market risk as credit activities generally span a longer time period.

II. Credit losses in the banking book should be assessed on the basis of mark-to-market mode as opposed to the default-only mode.

III. The confidence level used in the calculation of credit capital is high when the objective is to maintain a high credit rating for the institution.

IV. Credit capital calculations for securities with liquid markets and held for proprietary positions should be based on marking positions to market.

- A. I, III and IV

- B. I and III

- C. II and III

- D. I and II

Answer: A

Explanation:

Statement I is correct as credit VaR calculations often use a one year time horizon. This is primarily because the cycle in respect of credit related activities, such as loan loss reviews, accounting cycles for borrowers etc last a year.

Statement II is false. There are two ways in which loss assessments in respect of credit risk can be made:

default mode, where losses are considered only in respect of default, and no losses are recognized in respect of the deterioration of the creditworthiness of the borrower (which is often expressed through a credit rating transition matrix); and the mark-to-market mode, where losses due to both defaults and credit quality are considered. The default mode is used for the loan book where the institution has lent moneys and generally intends to hold the loan on its books till maturity. The mark to market mode is used for traded securities which are not held to maturity, or are held only for trading.

Statement III is correct. The confidence interval, or the quintile of losses used for maintaining credit ratings tends to be very high as the possibility of the institution's default needs to be remote.

Statement IV is correct too, for the reasons explained earlier.

NEW QUESTION # 145

In respect of operational risk capital calculations, the Basel II accord recommends a confidence level and time horizon of:

- A. 99.9% confidence level over a 1 year time horizon

- B. 99% confidence level over a 1 year time horizon

- C. 99% confidence level over a 10 year time horizon

- D. 99.9% confidence level over a 10 day time horizon

Answer: A

Explanation:

Choice 'd' represents the Basel II requirement, all other choices are incorrect.

NEW QUESTION # 146

There are three bonds in a diversified bond portfolio, whose default probabilities are independent of each other and equal to 1%, 2% and 3% respectively over a 1 year time horizon. Calculate the probability that none of the three bonds will default.

- A. 0.0006%

- B. 94%

- C. 0.11%

- D. 2%

Answer: B

Explanation:

The probability that only none of the three bonds will default is equal to the probability of all surviving. Since default correlation is zero, we can simply multiply the probabilities of survival. Therefore the correct answer is 94% = (1 - 1%) * (1 - 2%) * (1 - 3%)

NEW QUESTION # 147

The sensitivity (delta) of a portfolio to a single point move in the value of the S&P500 is $100. If the current level of the S&P500 is 2000, and has a one day volatility of 1%, what is the value-at-risk for this portfolio at the 99% confidence and a horizon of 10 days? What is this method of calculating VaR called?

- A. $4,660, parametric VaR

- B. $4,660, Monte Carlo simulation VaR

- C. $14,736, historical simulation VaR

- D. $14,736, parametric VaR

Answer: D

Explanation:

If the current level of the S&P 500 is 2000, and a single day volatility is 1%, and the delta (ie change in portfolio value from a one point change) is $100, then the 1 day volatility for the portfolio in dollars is 2000 *

1% * $100 = $2,000.

At the 99% confidence level, the value of the inverse cumulative density function for the normal distribution is 2.33 (=NORMSINV(99%), in Excel). Therefore the 1 day VaR will be 2.33 * $2000 = $4,660. Extending it to 10 days using the square root of time rule, we get the 10 day VaR as equal to SQRT(10)*4660 = $14,736.

Since this method of calculating VaR relies upon a delta approximation of a risk factor (in this case the S&P500), it is the parametric approach to calculating VaR (the other methods being historical simulation, and Monte Carlo simulation).

The 2015 Handbook provides an excellent example of parametric (and other) VaR calculations in Chapter 3 of Volume III of Book 3. The spreadsheet used for the illustration can be downloadedfrom

http://www.prmia.org/prm-exam/handbook-resources.

NEW QUESTION # 148

Which of the following is not an approach used for stress testing:

- A. Hypothetical scenarios

- B. Monte Carlo simulation

- C. Algorithmic approaches

- D. Historical scenarios

Answer: B

Explanation:

Choice 'c' is the correct answer as Monte Carlo simulations are not used to generate stress scenarios. They are applicable to VaR calculations under certain situations, and are not used for stress tests. The other three represent valid approaches to stress testing.

NEW QUESTION # 149

Which of the following statements is true in relation to collateral management?

I. A collateral management system need not consider the failure by counterparties to returncollateral when due II. The extent to which counterparties may have rehypothecated collateral is not a consideration for a collateral management system III. Cash is an acceptable substitute for any type of collateral required to be posted IV. Haircuts do not apply to treasury issued instruments posted as collateral

- A. I, II and III

- B. II and III

- C. None of the statements is true

- D. I, II, III and IV

Answer: C

Explanation:

Strong management of collateral, both receivable and payable, is emerging as an area requiring significant investment by financial institutions and asset managers in IT infrastructures and business processes. A bank needs to make collateral calls daily, based upon the P&L of the previous day, and likewise receives collateral calls from its counterparties. Just like cash, a bank needs to make sure that it does not run out of collateral to post when a call is received. Interestingly, based upon the agreements between banks and their mutual understanding, only certain types of instruments often qualify as valid collateral - and in such cases even cash is not acceptable if the right type of bond or other agreed security is not available to post. The operational challenges of managing collateral increase manifold due to 'rehypothecation', ie when collateral received from one counterparty gets posted out as collateral where it is due. In such cases, the bank should have the mechanisms to receive the right assets back in a timely way in case rehypothecated assets are to be returned.

The systems should be able to deal with delays, failures without impacting the ability of the bank to post collateral as needed. All of this requires major investments in IT and processes.

Statement I is not true as a bank is bound to post collateral to third parties when needed regardless of the failure of its counterparties to post collateral to it when owed. In the markets, failures by counterparties can and do happen, and a collateral management system needs to account for and keep a buffer for the fact that some collateral when due will not be received.

Statement II is not true as rehypothecation by counterparties of collateral posted increases the chances of the collateral not being received in time. The system should consider the need for liquidity to generate assets that can be posted as collateral when others have failed to return the collateral in a timely way.

Statement III is not correct as cash may not be acceptable to counterparties as collateral. From a practical point of view, they may not have the infrastructure to receive and account for cash as collateral. A Swiss bank, for example, may have an 'account' to receive US t-bills as collateral but may not even have a US dollar account to receive cash. Even if it did, the volumes of transactions going back and forth may make tracking and reconciliations impossible. Thus a bank should always make sure that it has the right type of collateral available to post.

Statement IV is incorrect as well, as treasury issued instruments are also subject to haircuts. Their value also fluctuates in response to changes in yields, and therefore they are subject to haircuts as well.

Thus none of the statements are correct and Choice 'd' is the correct answer.

NEW QUESTION # 150

Credit exposure for derivatives is measured using

- A. Forward looking exposure profile of the derivative

- B. Notional value of the derivative

- C. Current replacement value

- D. Standard normal distribution

Answer: A

Explanation:

Current replacement values are a very poor measure of the credit exposure from a derivative contract, because the future value of these instruments is unpredictable, ie is stochastic, and the range of values it can take increases the further ahead in the future we look. Therefore it is common for credit exposures for derivatives to be measured using forward looking exposure profiles, which are distributions of the expected value of the derivative at the time horizon for which credit risk is being measured. To be conservative, a high enough quintile of this distribution is taken as the 'loan equivalent value' of the derivative as the exposure. Choice 'c' is the correct answer.

The notional value of derivative contracts generally tends to be quite high and unrelated to their economic value or the counterparty exposure. Therefore notional value is irrelevant.

NEW QUESTION # 151

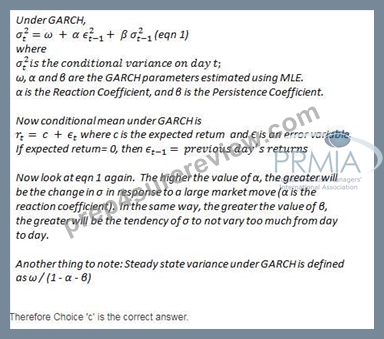

As the persistence parameter under GARCH is lowered, which of the following would be true:

- A. The model will react slower to market shocks

- B. High variance from the recent past will persist for longer

- C. The model will give lower weight to recent returns

- D. The model will react faster to market shocks

Answer: D

Explanation:

The persistence parameter, #, is the coefficient of the most recent day's returns in GARCH calculations. A higher value of the persistence parameter tends to 'persist' the prior value of variance for longer. Consider an extreme example - if the persistence parameter is equal to 1, the variance under GARCH will never change in response to returns.

A white text with black text Description automatically generated

NEW QUESTION # 152

For a FX forward contract, what would be the worst time for a counterparty to default (in terms of the maximum likely credit exposure)

- A. Right after inception

- B. Indeterminate from the given information

- C. Roughly three-quarters of the way towards maturity

- D. At maturity

Answer: D

Explanation:

With the passage of time, the range of possible values the FX contract can take increases. Therefore the maximum value of the contract, which is when the credit risk would be maximum, would be at maturity.

(Note that this is different than an interest rate swap whose value at maturity approaches zero.) Therefore Choice 'a' is the correct answer and the others are incorrect.

NEW QUESTION # 153

Under the standardized approach to calculating operational risk capital under Basel II, negative regulatory capital charges for any of the business units:

- A. Should be offset against positive capital charges from other business units

- B. Should be excluded from capital calculations

- C. Should be included after ignoring the negative sign

- D. Should be ignored completely

Answer: A

Explanation:

According to Basel II, in any given year, negative capital charges (resulting from negative gross income) in any business line may offset positive capital charges in other business lines without limit. Therefore Choice 'b' is the correct answer.

NEW QUESTION # 154

Company A issues bonds with a face value of $100m, sold at issuance at $98. Bank B holds $10m in face of these bonds acquired at a price of $70. What is Bank B's exposure to the debt issued by Company A?

- A. $10m

- B. $7m

- C. $9.8m

- D. $6.86m

Answer: B

Explanation:

Bank B's exposure is measured by the price it paid for the bonds, which in this case is $7m ($10m x 70/100).

Hence Choice 'c' represents the correct answer.

(Note that the question is asking for 'exposure' and not the legal claim in the event of default. The legal claim in the event of default would be the full notional of $10m. ) The initial issue price and issue size are irrelevant.

NEW QUESTION # 155

Which of the following statements is true in relation to a normal mixture distribution:

I. Normal mixtures represent one possible solution to the problem of volatility clustering II. A normal mixture VaR will always be greater than that under the assumption of normally distributed returns III. Normal mixtures can be applied to situations where a number of different market scenarios with different probabilities can be expected

- A. I, II and III

- B. II and III

- C. III

- D. I and II

Answer: C

Explanation:

Normal mixtures address fat or heavy tails, not volatility clustering. Therefore statement I is not correct.

Statement II is not correct. Where VaR is calculated at low levels of confidence, VaR based on normal mixtures may be lower than that under a normal assumption. This is no different than for other fat tailed distributions.

Statement III is correct. In situations where multiple market scenarios can unfold with a given probability, and each scenario is normal, we can express the result with a normal mixture where the underlying normal distributions have the probabilities of the different scenarios.

NEW QUESTION # 156

As part of designing a reverse stress test, at what point should a bank's business plan be considered unviable (ie the point where it can be considered to have failed)?

- A. When the regulatory capital of the bank has been exhausted

- B. Where EBITDA for the year is forecast to be negative

- C. When the realization of risks leads market participants to lose confidence in the bank as a counterparty or a business worthy of funding

- D. Where large known losses have been incurred on the bank's positions

Answer: C

Explanation:

As part of a reverse stress test, a firm has to identify and assess the scenarios most likely to cause it to fail, or in other words using the language used by the FSA in the UK, for its current business plan to become unviable. A firm's business plan should be considered to become unviable at the point that crystallizing risks cause the market to lose confidence it it, with the consequence that counterparties and other stakeholders are unwilling to transact with it or provide capital to the firm and, where releant, that existing counterparties may seek to terminate their contracts. Recent experience suggests that this point is reached well before a firm's regulatory capital is exhausted.

Large known losses, or negative EBITDA (earnings before interest , tax, depreciation and amortization) may be indicators or contribute to the loss of confidence, but do not of themselves make the current business plan unviable. Therefore Choice 'd' is the correct answer.

NEW QUESTION # 157

Which of the following is not a possible early warning indicator in relation to the health of a counterparty?

- A. Negative publicity

- B. A decline in the counterparty's corporate debt yield

- C. Credit rating downgrade

- D. Falling stock price

Answer: B

Explanation:

Negative publicity, a downgrade in the credit rating, a falling stock price are all pointers to potential credit problems, and the counterparty credit monitoring group of a bank should be using these as possible early indicators of an upcoming credit health problem. A decline in the yield of the debt issued by a counterparty means its spread is declining and the health of the credit is actually improving. Therefore a decline in the counterparty's corporate debt yield cannot be used as an indicator of potential credit problems.

Choice 'c' is therefore the correct answer.

NEW QUESTION # 158

For a corporate issuer, which of the following can be used to calculate market implied default probabilities?

I. CDS spreads

II. Bond prices

III. Credit rating issued by S&P

IV. Altman's scoring model

- A. I, II and III

- B. I and II

- C. II and III

- D. III and IV

Answer: B

Explanation:

Generally, the probability of default is an input into determining the price of a security. However, if we know the market price of a security, we can back out the probability of default that the market is factoring into pricing that security. Market implied default probabilities are the probabilities of default priced into security prices, and can be determined from both bond prices and CDS spreads. Credit ratings issued by a credit agency do not give us 'market implied default probabilities', and neither does an internal scoring model like Altman's as these do not consider actual market prices in any way.

Therefore Choice 'b' is the correct answer and the others are not.

NEW QUESTION # 159

Under the contingent claims approach to measuring credit risk, which of the following factors does NOT affect credit risk:

- A. Leverage in the capital structure

- B. Cash flows of the firm

- C. Maturity of the debt

- D. Volatility of the firm's asset values

Answer: B

Explanation:

Under the contingent claims approach, credit risk is modeled as the value of a put option on the value of the firm's assets with a strike equal to the face value of the debt and maturity equal to the maturity of the obligation. The cost of credit risk is determined by the leverage ratio, the volatility of the firm's assets and the maturity of the debt. Cash flows are not a part of the equation. Therefore Choice 'a' is the correct answer.

NEW QUESTION # 160

For identical mean and variance, which of the following distribution assumptions will provide a higher estimate of VaR at a high level of confidence?

- A. A distribution with kurtosis = 8

- B. A distribution with kurtosis = 3

- C. A distribution with kurtosis = 0

- D. A distribution with kurtosis = 2

Answer: A

Explanation:

A fat tailed distribution has more weight in the tails, and therefore at a high level of confidence the VaR estimate will be higher for a distribution with heavier tails. At relatively lower levels of confidence however, the situation is reversed as the heavier tailed distribution will have a VaR estimate lower than a thinner tailed distribution.

A higher level of kurtosis implies a 'peaked' distribution with fatter tails. Among the given choices, a distribution with kurtosis equal to 8 will have the heaviest tails, and therefore a higher VaRestimate. Choice 'a' is therefore the correct answer. Also refer to the tutorial about VaR and fat tails.

NEW QUESTION # 161

Which of the following statements is true:

I. Confidence levels for economic capital calculations are driven by desired credit ratings II. Loss distributions for operational risk are affected more by the severity distribution than the frequency distribution III. The Advanced Measurement Approach (AMA) referred to in the Basel II standard is a type of a Loss Distribution Approach (LDA) IV. The loss distribution for operational risk under the LDA (Loss Distribution Approach) is estimated by separately estimating the frequency and severity distributions.

- A. I, III and IV

- B. I and II

- C. III and IV

- D. I, II and IV

Answer: D

Explanation:

Statement I is correct. Economic capital is the capital available to absorb unexpected losses, and credit ratings are also based upon a certain probability of default. Economic capital is oftencalculated at a level equal to the confidence required for the desired credit rating. For example, if the probability of default for a AA rating is

0.02%, then economic capital maintained at a 99.98% would allow for such a rating. Economic capital set at a

99.8% level can be thought of as the level of losses that would not be exceeded with a 99.8% probability.

Loss distributions are the product of the severity and frequency distributions, each of which are estimated separately. The total loss distribution is affected far more by the severity distribution than by the frequency distribution, therefore statement II is correct.

The Loss Distribution Approach (LDA) is one of the ways in which the requirements of the AMA can be satisfied, and not the other way round. Therefore statement III is incorrect.

Statement IV is correct as the total loss distribution is estimated using separate estimates of loss frequency and distributions.

NEW QUESTION # 162

......

Latest 8011 Exam Dumps - Valid and Updated Dumps: https://dumpstorrent.prep4surereview.com/8011-latest-braindumps.html