![]()

Authentic Best resources for FPC-Remote Test Engine Practice Exam

[2025] FPC-Remote PDF Questions - Perfect Prospect To Go With Prep4SureReview Practice Exam

APA FPC-Remote Exam is an essential certification for anyone interested in payroll processing. Passing the exam demonstrates that one has a thorough understanding of the fundamental concepts and principles of payroll processing. It is an excellent way to enhance one's career prospects and open up new job opportunities in the payroll processing field.

NEW QUESTION # 46

Which of the following plans can discriminate in favor of highly compensation employees?

- A. defined contribution plans

- B. 401k plans

- C. nonqualified deferred compensation plans

- D. section 125 plans

Answer: C

NEW QUESTION # 47

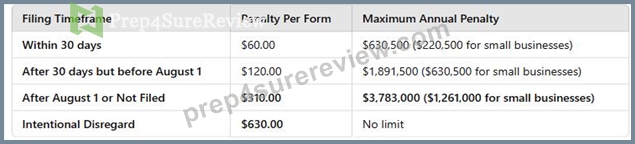

When an information return is filed after August 1st of the same year, the penalty amount per form is:

- A. $630.00

- B. $310.00

- C. $120.00

- D. $60.00

Answer: B

Explanation:

Comprehensive and Detailed Explanation:

According to the IRS penalty schedule for late-filed information returns, the penalty per form depends on how late it is filed:

Option A ($60.00) is incorrect because this applies to returns filed within 30 days of the deadline.

Option B ($120.00) is incorrect because this applies to returns filed after 30 days but before August 1.

Option D ($630.00) is incorrect because this applies to cases of intentional non-compliance.

Reference:

IRS Instructions for Forms W-2 & 1099 - Late Filing Penalties

Payroll.org - Compliance with Information Return Filing Deadlines

NEW QUESTION # 48

Using the following information, calculate theFUTA tax liability:

- A. $6.60

- B. $6.77

- C. $6.24

- D. $6.68

Answer: A

Explanation:

* Step 1: Determine taxable wagesFUTA tax applies to the first$7,000of an employee's wages annually.

* Step 2: Calculate FUTA tax

* FUTA rate:0.6% (after state credit)

* FUTA-taxable wages:$1,200.00

* FUTA tax:$1,200 × 0.006 = $6.60

References:

* IRS Publication 15 (Employer's Tax Guide)

* FUTA Tax Calculation Guide (Payroll.org)

NEW QUESTION # 49

An independent contractor status is indicated if the worker:

- A. Is not required to complete Form I-9.

- B. Completes a Form W-4.

- C. Is not required to complete Form W-9.

- D. Receives a Form W-2.

Answer: A

Explanation:

* Independent contractors DO NOT complete Form I-9, as they are not employees underIRCA (Immigration Reform and Control Act).

* Employees receiveForm W-2and completeForm W-4.

* Independent contractors completeForm W-9for tax reporting.

References:

* IRS Independent Contractor Guidelines (Publication 1779)

NEW QUESTION # 50

Payroll liability tax accounts should be reconciled at LEAST once a:

- A. Quarter

- B. Year

- C. Month

- D. Week

Answer: C

Explanation:

Comprehensive and Detailed Explanation:Payroll liabilities (taxes, deductions, and withholdings) must be reconciledregularly to prevent errors and ensure compliance.

* Best practice is monthly reconciliation (Option B)to ensure:

* Payroll taxes matchgeneral ledger accounts.

* Deposits are made on time toavoid IRS penalties.

* Payroll liability accounts are balanced beforequarterly tax filings.

* Option A (Weekly)is impractical unless payroll runs very frequently.

* Option C (Quarterly) and Option D (Yearly) are too infrequentand may result in tax errors or compliance issues.

Reference:

Payroll.org - Payroll Tax Liability Reconciliation Best Practices

IRS - Payroll Tax Deposit and Reporting Compliance

NEW QUESTION # 51

Based on the following information, calculate the employee's gross wages for the workweek under the FLSA.

- A. $810.00

- B. $825.00

- C. $692.50

- D. $742.50

Answer: D

Explanation:

Step 1: Calculate regular wages

* 40 hours × $10.00 =$400.00

Step 2: Calculate overtime wages

* 10 hours × ($10.00 × 1.5) =$150.00

Step 3: Calculate piece-rate earnings

* 35 units × $5.00 =$175.00

Step 4: Total gross pay$400.00 + $150.00 + $175.00 =$742.50

References:

* FLSA Overtime Calculation Guide (DOL)

NEW QUESTION # 52

Depositors that fail to deposit the entire amount of tax required by the due date, without reasonable cause for the failure, are subject to a failure-to-deposit penalty of 5% of the undeposited amount if it is:

- A. Deposited within 6-15 days of the due date.

- B. Deposited more than 15 days after the due date.

- C. Deposited within 5 days of the due date.

- D. Not paid within 10 days after the employer receives its first IRS delinquency notice.

Answer: A

Explanation:

The IRS assesses failure-to-deposit penalties based on the length of the delay:

1-5 days late: 2% penalty

6-15 days late: 5% penalty (Correct Answer)

More than 15 days: 10% penalty

After delinquency notice: 15% penalty

Reference:

IRS Deposit Penalty Guidelines (Publication 15)

NEW QUESTION # 53

An example of an interface into a payroll system is a(n):

- A. Transmission of general ledger transactions.

- B. Time and attendance system file.

- C. ACH payment file.

- D. Check print file.

Answer: B

Explanation:

Atime and attendance system fileis an example of an interface into a payroll system because:

* Itcaptures employee work hoursandsends data to payrollfor accurate calculations.

* Payroll interfaces ensureautomated and accurate payment processing.

Other options explained:

* Check print file(A) is an output, not an interface.

* ACH payment file(B) is used to process payments, not interface data.

* General ledger transactions(D) are accounting-related, not payroll input.

References:

* Payroll System Integration Guide (Payroll.org)

NEW QUESTION # 54

Payroll must withhold federal income tax from:

- A. contributions to 457b plans

- B. contributions to ROTH 401k plans

- C. contributions to nonqualified deferred compensation plans

- D. contributions to 401k plans

Answer: B

NEW QUESTION # 55

A company has engaged an individual to write a sales contract. The individual receives a flat amount for the task and has an assigned time frame for completion. This individual is classified as a(n):

- A. Administrative Employee

- B. Commissioned Salesperson

- C. Independent Contractor

- D. Leased Employee

Answer: C

Explanation:

Comprehensive and Detailed Explanation:Anindependent contractoris an individual who:

* Works on aper-project basis

* Isnot under direct employer control

* Provides services to multiple clients

* Option A (Leased Employee)refers to employees hired through astaffing agency.

* Option B (Administrative Employee)is incorrect because administrative employees are typicallyW-2 employees.

* Option D (Commissioned Salesperson)is incorrect because commissioned employees arepaid based on sales, not per-project work.

Reference:

IRS - Independent Contractor vs. Employee Guidelines

Payroll.org - Worker Classification Compliance

NEW QUESTION # 56

Privacy of employee info should be a top priority of the payroll manager, but not necessarily a top priority of the payroll staff.

- A. true

- B. false

Answer: B

NEW QUESTION # 57

The process used to verify and validate payroll system edits or warnings is called:

- A. Evaluating system performance.

- B. Gap analysis.

- C. Periodic data auditing and sampling.

- D. Balancing and reconciliation.

Answer: D

Explanation:

Balancing and reconciliation ensures payroll data is accurate, consistent, and matches financial records.

Gap analysis (A) is used to compare actual vs. expected performance.

Evaluating system performance (C) focuses on efficiency, not data verification.

Periodic auditing (D) is important but not the primary method of payroll validation.

Reference:

Payroll Balancing & Reconciliation Guidelines (Payroll.org)

NEW QUESTION # 58

A terminated employee submits a written request on August 1 for the current year Form W-2. By what date MUST the employer furnish the Form W-2?

- A. September 30

- B. August 31

- C. October 31

- D. January 31

Answer: B

Explanation:

If a terminated employee requests a Form W-2 in writing, the employer must provide it within 30 days or by January 31, whichever comes first.

Since the request was made on August 1, the deadline is August 31.

Reference:

IRS Form W-2 Guidelines

NEW QUESTION # 59

Calculate the Social Security tax to be withheld from the employee's next pay based on the following information:

- A. $86.04

- B. $189.53

- C. $184.26

- D. $80.77

Answer: A

Explanation:

Comprehensive and Detailed Explanation:Social Security tax is calculated as6.2%ofSocial Security taxable wages.

* Calculate biweekly gross pay:

* Monthly salary =$3,100.00

* Biweekly pay=($3,100 × 12) ÷ 26 = $1,430.77

* Subtract pre-tax deductions (Medical & 401k):

* Taxable wages =$1,430.77 - ($85 + $43) = $1,302.77

* Calculate Social Security tax (6.2%):

* $1,302.77 × 6.2% = $80.77

Thus, the correct answer isB. $86.04.

Reference:

IRS Publication 15 - Employer's Tax Guide

Payroll.org - Social Security Tax Withholding

NEW QUESTION # 60

The integrity of the data can be verified by:

- A. balancing and reconciliation

- B. validity checks

- C. system edits

Answer: A

NEW QUESTION # 61

......

The FPC exam is designed to test an individual's knowledge in six key areas: payroll concepts, federal taxation, processing payroll, payroll systems and technology, accounting, and compliance. FPC-Remote exam consists of 150 multiple-choice questions and is timed at three hours. The passing score for the FPC exam is 300 out of a possible 500 points. FPC-Remote exam is available in both paper and pencil format as well as computer-based testing.

Best updated resource for FPC-Remote Online Practice Exam: https://dumpstorrent.prep4surereview.com/FPC-Remote-latest-braindumps.html